So a lot of blogs suggest: pick an airline, pick a hotel and stick with those programs. The downside of this approach is that you are tied to them. You are tied to their schedules and hotel availability. And that is no freedom. Or fun. You want to experience the real matrix of having the flexibility to book anytime or time of your convenience and choose to reside at a place of your comfort. This relates to a recent experience of my flying between NYC and LA. Often times with a fixed airline and hotel approach I found that there were moments of anxiety around availability. This got somewhat mitigated as I expanded to other hotels and flight programs. This not only allowed to get cards from different banks and try them out and accumulate points in different places, but it also builds up a steady balance of diversification across various brands and thus gives you the freedom to choose geography over the math of limited choices. Hence, my strategy is now revised to go all out in o(n) fashion in just accumulating points after points from various banks. Just going all out also gives you this satisfaction that you have really tried out all available options out there. Just like in a buffet. Having said that, there are some default programs that are and should be the basis of this activity. I would say in airlines that would be Southwest and United. These are two solid airlines that cover US and good parts of this world like Asia that one would want to visit often. Of course there is Delta and American and Jetblue and others. For reason unknown I tend to avoid Delta while American is fine or Jetblue is cool and same with say, Frontier. Dont get me wrong. I am not against them. But the base is Southwest for me. There are plenty of them alright and many other airlines which are rather really good to travel and experience. Etihad or Emirates or Singapore Airlines or Cathay Pacific among others are all solid and so are national carriers of many countries (except China and Chinese airlines, avoid them at all cost!) . Same goes with Hotels. I like Marriot or Starwood a lot. Hilton is not bad too. IHG is good and their branded card is really worth the $49 annual cost since you are not going to find a hotel room anywhere in the US in one of the IHG hotels like Holiday Inn for 49 bucks a night. I used mine in the Big Island Hawaii! :D .. one of the best night stay ever! So the revised strategy is really avoid rental cars loyalty programs, go all out and apply one by one to each hotel and air cards and keep some of those that you like even if they charge you annual like the southwest cards or the marriott cards or IHG cards. And apply Starwood or Amex cards once every couple years.

Wednesday, October 12, 2016

Current Credit Card offers..

To keep up with the point of this blog, some good current offers are:

- American Express Platinum and Enchanced Business Platinum Card: This card has an annual fee of $450 so be careful. However, they also reimburse the portion should you cancel it earlier unlike Citi and Chase who do not. The funny thing is both Citi and Chase seem to hold a grudge should you cancel their paid credit cards as if you owe them that and that impacts your future credit cards applications in those banks. Amex is overall a bit cooler in that respect. I would say one platinum card per 2 years is not that bad to your relationship with Amex or your overall credit score health. This remains the best $450 card and the best in its league. Apart from the always dependable Customer service experience with Amex, the best thing is the $200 annual rebates, the unparalleled lounge access and the best offers floating around this time of the year. There is an unprecedented 100k offer here, visible right on the American Express website. The spending requirement is steep however at $15k. There are also offers of 75k points with $5k spend.

- Chase Sapphire Reserve: The splashy card and a much hyped one for the last month or two, this is another $450 card but with same 100k offer as the Amex platinum card. A big plus is the $300 annual travel credit on any airline. Now that is a big benefit. However, the big downside is the strict rules in applying, the so called 5/24 rule which makes Chase deny any applications if you had applied for 5 credit cards anywhere in the last 24 months, rendering it useless to most people. That said, again $450 annual fee? That is too much. It is a decent card nevertheless. There are questionable lounge access features and does not seem to carry the same weight if you are looking for prestige or if you are into all that.

- Citi Prestige card: Well, this card is dead. They downgraded the offer to 20k points. And with this, this card is simply not attractive enough. At the point of the release of this card last year, I had penned a post about how really silly it is to spend $450 on a credit card which one would normally not do even if it justifies some value in giving you back points. I still stand by the same and would expand on that briefly.

Most other cards did not top the above and were giving out anywhere in the equivalent of $100 to $400 - the latter being Barclays Arrival+ card. Amex and Chase are clearly duking it out in 2016 with Citi contended to sit back after the hit in Prestige from last year. For most of this year, Citi and the rest have been at the back. Amex and Chase upped their hotel game with Ritz card changes and Hilton Card changes. Amex went with a Delta platinum version which based on comments on Reddit and other online sites, seems to be a big hit with the Delta travellers. Mind you, a good chunk of Delta fliers are either Government workers or regular consultants who commute Monday - Thursday.

The perils of an annual fee card: This is not for sub 100 annual fee card which still even if more is not as insane as the $450-$500 that the big "reserve" or "platinum" cards charge. Admittedly, I had applied for few of those in the past. With platinum, I always close after some period, ideally within 30-60 days. Chase Reserve also has a grace period of 60 days if that is something that they grudgingly will record against you. But the point that the other bloggers push is the value that you get out it. What value ??? Most likely you were not even thinking of travelling or taking that hotel or air fare in first place. If at all you do there is still generic branded cards ? You could always find and make money or points with your normal spend in no fee to sub-100 fee cards. So is it really some sort of high or this rush that is there with the sudden 50k or 100k bonuses? Obviously, if there is no 50k+ offer, no one is going to look twice at these cards. But even with that, are they really worth it?? I would say no. I regret paying and holding Citi prestige for a year and cancelled it despite their various offers and attempt to shell 450 for another year. I did get the 200 * 2 credit and 50k points. I took trips to Hawaii and got rentals based on that. I would deny that. But it is essentially the 450 that I paid from my pocket which contributed to a part of it. Bear in mind, that many also have a steep spending requirements. Chase Reserve has the 5k spend but they tend to have all these useless categories where they keep inducing you to spend more. I would not have really gone to that restaurant but hey, some one is giving me 5% cashback so why not try it .. really that is just 5 bucks on a 100 bucks bill. Anyhow, if I were to recommend, I would say no to Citi for sure. Maybe once give it a try to get a feeling of it and get some rewards but no point in doing it again. For chase, maybe no unless like citi you plan to keep it a whole year. For Amex, see if you are a good client with their regular cards and if you do this once every 2/3/4 years I would doubt they would seriously mind that much. In the past I have had the mercedes benz as well as the platinum card and both were closed soon. Given that Amex is the best credit card issuer and has been for quite some time, make sure that the bridges are not burned. Chase though good is a clear distant second and not to mention the rules there are getting stricter. The Citis and Bank of Americas or the rest are there but better to stick with the best.

October updates

Phew! After a long time !! There was barely any excitement in the credit card space to merit a writing these days. First off, the days of limited time deals are gone as most offers are only with big banks who offer a rather huge window to apply. Further, the rules of the game have been tightened so far that now only legitimate spenders are applying for cards since the avenues to spend artificially has reduced exponentially. So some general updates:

- Many prepaid accounts such as Amex Serve or Bluebird or from other companies are practically gone or dead. The ones remaining are used for their primary purposes and are being viewed with hawkeyes.

- Most gift card methods are hence a dead game now. There are some vanilla gift cards and other cards which can be used to meet those high spending requirements but overall, many are gone. Paypal and the big ones were anyway dead so now they are not all being used by anyone in the spending community.

- The spending threshold is increasing and many banks are not afraid to ask you to spend upward of 10 grand, yes 10 grand!, before you see some good long term benefits.

- This is not a very long term strategy if you could call that .. rather it is something that one does on the side, as a hustle maybe? as long as the expectation is set that it is something that gives yo some play money rather than anything concrete.

The current big bonus cards are all having steep annual fees which are not waivable. Take for instance, Chase Sapphire Reserve card. At $450 annual fee that is not waived, it is by no means a cheap card. The argument that you can recoup this fee in rewards is extremely silly. I want to travel then I travel and not the other way round that you have some $300 gift card and hence you travel anyway to New York or some big city. That is really silly. In a way, one can clearly see that it induces spending. Had there been no rewards, would you really spend $450 on a credit card ? I mean seriously, for fuck's sake, how many can sanely think that you are going to spend $450 on a credit card ?? Anyways.

So in all, I see that this space is shrinking which reflects in lesser blog entries for this blog. Now, if you really follow the main blogs in this space, you would notice that they are all moving away from just credit card blog to broader "financial" blog and also advertise any amount of things .. they could say it is travel blog but they also cover a whole lot of ground other than travel tips or credit card tips. They do generate a lot of hype since they are anyways affiliates of big banks unlike this blog.

The downside of all this is that the banks have now realized that they can up the game and really come up with products that have high premiums and fees and dole out some points for air travel or hotel points. For the regular customer anyways, this is a far cry from anything that they use the credit card for.

Friday, June 3, 2016

New Credit Cards

So the current list of credit cards which are with good bonus points:

- Chase Marriott - Business and then Personal

- American Express Delta

- American Express Starwood - try to get this asap before the Mariott-SPG Merger

- Chase Continental - back to 50k points

- Chase Ink+ Business Card

That is pretty much it.

I have been trying to gather more info about City National Bank. This is a regional bank credit card for mostly people in the Hollywood region - so that is SoCal with ties to entertainment industry. They seem to have a pretty nice card with great features and bonuses. More on this later!

Tuesday, May 24, 2016

May June 2016 Credit Cards

For May and June 2016, the credit card blogroll is lead by Chase Bank.

Chase has some good cards up their sleeve like the Marriott Card and Chase Ink Card.

The Business version of the Marriott card is offering the best bonus of any card for any hotel across the previous decade:

https://creditcards.chase.com/credit-cards/marriott-business-credit-cards.aspx?CELL=6TKV

That is a direct link to the bank site and this site is not an affiliate with Chase or any other bank or any affiliate company.

The personal version of this credit card offers about 80,000 points.

The Chase Ink card is also a versatile card that offers 60,000 points. Both these cards have no annual fee waived for the first year.

Is it worth it?

I would highly recommend both these cards over any other card in the market right now for the bonus points and are definitely worth it.

Runner up is the Citi Cards - Prestige/American are still good.

Rest of the cards for this period is pretty much the same as it was earlier-Nothing exciting!

Chase has some good cards up their sleeve like the Marriott Card and Chase Ink Card.

The Business version of the Marriott card is offering the best bonus of any card for any hotel across the previous decade:

https://creditcards.chase.com/credit-cards/marriott-business-credit-cards.aspx?CELL=6TKV

That is a direct link to the bank site and this site is not an affiliate with Chase or any other bank or any affiliate company.

The personal version of this credit card offers about 80,000 points.

The Chase Ink card is also a versatile card that offers 60,000 points. Both these cards have no annual fee waived for the first year.

Is it worth it?

I would highly recommend both these cards over any other card in the market right now for the bonus points and are definitely worth it.

Runner up is the Citi Cards - Prestige/American are still good.

Rest of the cards for this period is pretty much the same as it was earlier-Nothing exciting!

Friday, April 29, 2016

Shoutouts

There are few blogs and sites which catch our attention and we subscribe to it and visit it daily to get the view points or rather monitor the trends in a particular space - say credit cards for this site, or finance for other sites or travel.

So some of the recommended sites in finance are:

http://millenialfinanceblog.blogspot.com/

https://millenialfinanceblog.wordpress.com/

Mr Money Moustache Blog

My Money Finance blog

For auto deals: There was only place that is worth recommending which is www.autoslash.com

There are multitudes of other apps in both Apple iOS and Android where you can download them and try for their features. They might not be really great and simply an extension of what your text. word or excel files does but it good to have them handy but to tune off the noise you are better off just putting them in a document and then transferring over to a calendar or task manager and execute them from there.

Tuesday, April 26, 2016

Credit Card Diet

April is almost over. Last weekend of this month! There are quite a bit of credit card offers swirming around: PNC Bank has a new credit card; Citi has cancelled a lot of their sign up bonuses; Chase has implemented stricter rules though the Chase Ink card is still available with 60k points or 70k points if you visit in branch and give them the business code; American Express has also tightened its hold; lot of regional and local ( city/state/county) specific credit unions have average offers coming up - the best way is to listen to the radio stations or just search for the local banks and then apply in their site directly. But all in all, this seems to be a time for a credit card diet!

Yes, this blog is going to be unique in advocating a credit card diet to most people out there. This thing has gone on for a while and like an obese person, many credit card appers have just binged on credit card apps willy nilly. And like an obedient restaurant, banks have served up the feast rather quite well. So now is the time to just cool off a bit, maybe run around in a beach or park, maybe go outside and do other activities .. or maybe just go shopping without thinking of a credit card. Wait! What is that ?? Well, it is the same free feeling that one used to get right after getting a job in their early 20s when all one could think was what to buy and what is the budget. While these days it is mostly which credit card to buy with and how much should be the spend etc. Just be free like the old days and go out and buy and have fun. Which is why we are celebrating the next few months as credit card diet months - a period of about 3-4 months when no matter what one is not going to apply for a new credit card. This will also be the time when the credit score will likely get back to higher ranges positioning you to better offers down the line. And the credit report will get a breather form incessant inquiries and you can review it as a silent period and bookmark it as a time when you did not have much activity going on.

In future, we will tend towards having at least a few months per year when there is no credit card app. And also the apps themselves will be in silos rather than just apping 10s of them on a single day. The reason being getting spaced out or edged out of this game as you accumulate more and more credit cards. The rules prevent you from getting too many points repeatedly and many banks will deny you points if you apply in the last 1-2 year. So all in all, this will become a more choosy game as times flies by.

Thursday, March 10, 2016

March 2016 updates

For credit cards bonus signups, this early period of 2016 has pretty much dried up many quick spending options that does not cost you much. Some good old strategies still run while the credit card issuers themselves have tightened up the belt.

Sample this:

Amex is no longer offering repeat sign on bonus for any of their cards - personal or business.

Chase has begun very strict approval of their cards. There goes the top bonuses.

Citi is also having strict card opening process and not giving any new big bonuses.

The rest of the pack all fall somewhere behind all this. Is it a logical end for the people in this blog space? Are they evolving to more of a finance blog rather than just travel or credit card blogs that they aspire to ? Many of them just put daily deals and "buy tickets to europe" or "buy tickets worth $1500 for $1000" or something like that. I think those are pretty much click bait or spend bait articles. Yeah, they will fulfill the basic contractual obligation of having to publish at least 1 article per day as required by some affiliates and advertisers. It might require you to publish some images and silly captions under the guise of some informative article but cut thru the noise and it is just empty. In this blog, we vowed to never publish empty noise. If there are no deals, then no need to publish anything. We not depending on advertisers or affiliates gives this blog a rather independent and pure voice without bias. If there is good deal, we will publish it. No urgent deals or something that will require you to click on it and make a split second decision.

Some of the current deals that are worth looking:

Chase Slate card: The online version is pretty good.

Bank of America/Slate/Discover It/Capital One Quick Silver Spark One card: All of those are good for balance transfer offers.

Any Chase cards with Hotels: Fairmont and Hyatt are top of the line and better to apply them now given the tighter policies of Chase.

American Express Gold and Platinum: There are offers worth 50,000 points to 75,000 points directly from the bank site.

Few credit unions and banks have decent yet repetitive offers - nothing new.

That is it .. nothing else for now!

Wednesday, February 3, 2016

February 2016 credit card updates

So by now, most people would have heard about the recent change ups in the way Amex handles its prepaid cards such as Serve or Bluebird among others - the primary tool for those that want to increase the credit card spend. It was shut down massively across for many people and blogosphere erupted one fine day about so many cancellations. This method is all but over with those that persisting with spending via serve or bluebird or any similar cards just inviting it from the big banks to shut down their accounts. So whats left? Well, it is pretty much legitimate spending that is left! Never ever do manufactured spend or needless spending and in any case the system has caught up to those that do and really the only avenues left are using the credit cards for just and legit spends.

Now with that in mind, let us look at some good cards going on as of February 2016:

Chase Sapphire: Pretty good for new comers with 50k points bonus offer.

Chase Ink: For those with business, with 60k points.

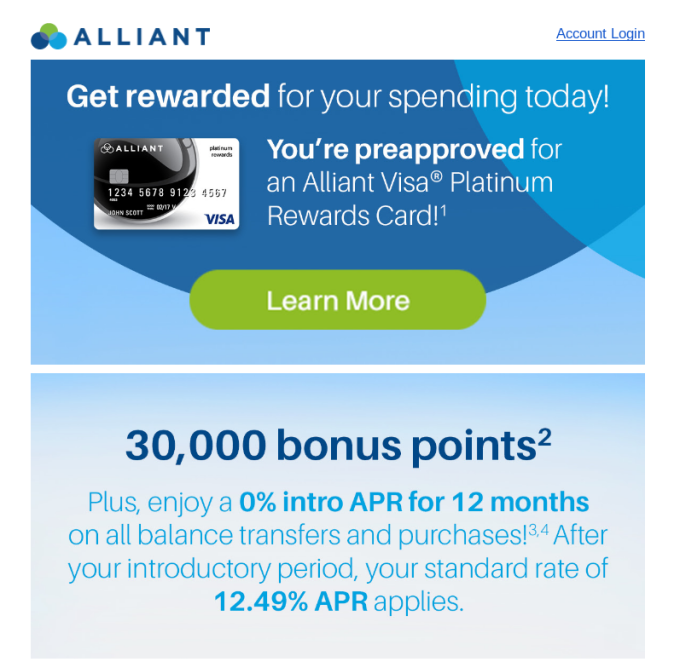

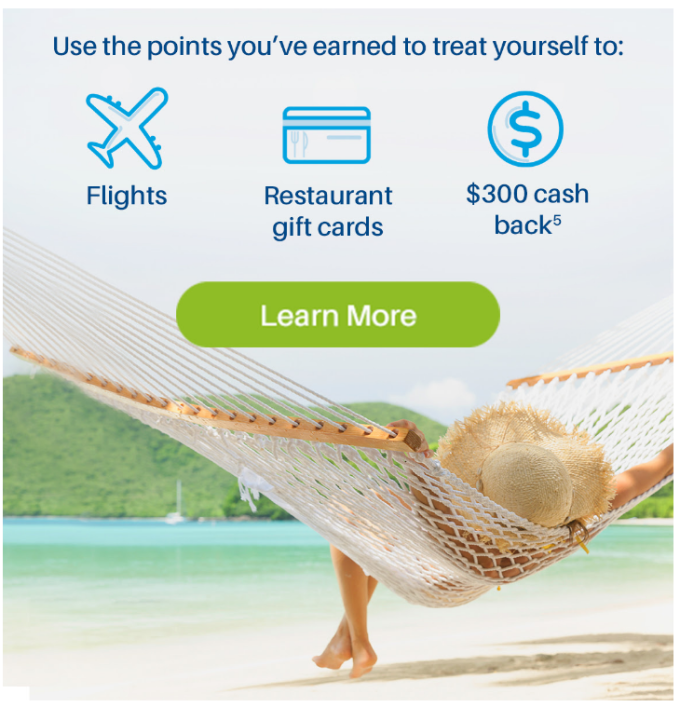

Alliant Credit Union: Yes, a credit union is finally coming up with something strong. They have one of the best offers right now with 30k points. Pretty high for very low spending requirement. Details below.

This is a pretty good deal. Lot of redemption options are there including cash back and booking for airlines. Details below:

The selection on gift cards are also very good on this site. And there is no fee on this card. So in all, a very good deal!

For Business users, Capital One has the Venture and Spark cards with 50k points offer.

There is also the better SimplyCash from Amex with about $250 bonus offer.

The rest of the cards are as listed in the top cards section of this website. No major changes so far in 2016. Let us see how this industry shapes up thru this year.

Friday, January 22, 2016

Annual Reports on Credits Cards, Airlines, Hotels and State of Travel.

So this small blog is by no means as big as some of the bigger agencies out there but we thought it would be a good idea to have an annual report sort of which summarizes not only 2015 but also gives some look ahead on things that one can expect in 2016. This is not extensively data oriented or nuanced but it is well researched and presents our views, opinions, ideas and our take on the state rather than present the reality perspective. However, for an average reader, this will give some sort of closure and a good perspective on not only 2015 but also the years that led up to it and how things will likely be in 2016.

Credit Cards:

The main idea of this blog is to maximize credit card spend and rewards using various automated or close to automated means which would also be simple. Now, in the past the leading candidate has mostly been American Express. Any agencies out there will usually put them at the top across various segments. Rewards, just like their customer service, is no different either. So if you really want to not have to deal with a lot of cards and have just one, go with one from this bank and you are in good stead. In 2015, though Amex still leads the rest, the rewards are strictly hohum. I would not recommend applying for any old cards or go after anything particularly new ones at the moment. Discover has caught on with equivalently good customer service but not at all a match to Amex when it comes to rewards. Chase was as usual good. Like Amex, if you want to have one card with wider acceptability like Visa and Mastercards with Secure pins to boot, go with Chase. In fact, I would say they are good to have in your wallet and credit report in general. There are lots of cons too which we have detailed elsewhere but overall Chase is a close runner up to Amex. Citi was the surprise kid in 2015. Now, for those in 2000s know that Citi was the front runner for many years but got shanked in the financial crisis and they suspended many programs and cut down on credits drastically. But 2015 was good for citi lineup with many decent cards. We argued that some are not necessary or just entice you to give in for high fees etc. Nevertheless, it was good for Citi. Is it that one card with one bank that you can go with? I would say no. That would still be Amex or Chase in general. But if you have to go with Citi for whatever reasons, that card without doubt would be the Citi Cashback 2% card. And that card can easily beat the best from Amex or Chase or rather anyone in the market at the moment. The only downside is no sign up bonuses here. Those are the big three. No major credit unions offers. Barclaycards continue to climb up the US credit card industry with more and more cards and good offers all around. They seem to be loosening up a bit after losing US Airways but have landed Jetblue likely. And they are good too. At least better than the ones below such as US Bank or Fidelity or MBNA or whatever. These banks continue to lag at the bottom.

Bank of America and its cards are still decent but dont expect anything out of this world. BBVA is a new kid in the block with good Amex/NBA partnerships. It is a good card for sports fans. Discover ran some interesting promotions. Capital One was Capital One. Still decent and conservative and an indicator of excellent credit. That is it!

Airlines:

The airline industry in 2015 had a good year overall but for customers the rewards could have been better. The miles earnings models are shifting to more revenue generation. Which means the credit card earning route is all the more valuable. But you have to know how and when to go with this route. Southwest leads the pack with best program and the best card in Chase southwest card. This is one card where one need not mind the fees at all. Jetblue is second with fantastic service but credit cards wise they need to really amp up the game. United is pretty good amongst the rest of the legacy carriers. American comes in after United and that is mainly because of the tie up with their partners British airways whose avios points are still good. Delta is as usual dead last and even if you pay for this bird, you are coming out pretty unsatisfied. Foreign carriers are interesting nice. A lot of them are pretty decent with miles but let us keep this domestic. Virgin America, Spirit, Airtran, Frontier et al are there and have decent programs. But where airlines differ from some other industries is that airline sector is mostly static and slow. Things dont change and are less inspirational. More competition is needed so that prices go down and rewards accumulate. Even if you look back in the last 10-15 years, this industry is not exactly the trend setter in its space or something that excites others.

Hotels:

Hyatt/Marriott/SPG/IHG are all pretty good and depends a lot on the location where you chose to avail their services. Lot of mergers and acquisitions happened and continue to do so. Hopefully this industry does not go the way of airlines and gets stuck in the stagnated route. New sites like Airbnb are really creating a dent in this market. Likely will continue to do so in 2016. A shout out for the Chase IHG card which is the only card with a free night for an annual fee of $49. It is pretty much the lowest of the hotel cards right now and we would recommend keeping this card if you are going to use a free night worldwide on IHG Chain which are pretty good with holiday inn and the likes.

Rental Cars:

As is the line of this blog, we dont focus much on rental cars loyalty programs per se. It is one of those perks that if its there or you get a 20% off coupon, one just uses it. A big shout out to autoslash - a pretty nice algorithm that keep aggregating relentlessly to find you the best rates over time. I wonder why no one is doing the same for the hotel industry at least because that would be super tough to achieve in the airlines world - not technically but for the closed nature of this industry. I guess hotel lobbyists would also jump too much in arms if there would be more openness to reservations systems of a hotel. Expect Uber, Lyft etc to dent into this market and chip in the share so hard that the car rental guys will have no option but to cave in with way lesser rates similar to what is happening to taxi unions.

That is it! Hope this give you some perspective on things. Travelling for work sucks in general. Unless it is a different location and hotel etc. That adds some varieties and spice to your work life. The same old scenary and same old cramped plane - week in and week out just jades you. I think one can reasonably do travelling for about 10-12 weeks before they need a break and settle down to a more regular work travel rhythm or a work from home routine. For travelling folks, it would be tough to keep track of miles and often the preference should rightfully be to get to and fro destinations quickly. Same with hotel and other things. A best case scenario that is also humane for a decent travelling worker usually involves about 20 flights and with revenue based model that would give about 10, 000 points. You could wish the best case scenario of this being a southwest flight. Essentially this points can be redeemed for one or two short haul flights. Too much inefficiency! Forget about rental cars and the best in class hotel would give you something like 1 night free for about 15 nights or so. Unless you have a card such as Citi Prestige which gives you 1 free night every 3 booked nights! But then you might run into billing issues there. But keeping these things aside, I think hotel industry is also not up there in terms of efficient way to earn miles.

All of this pretty much lays emphasis on the need to use credit cards strategically, now more than ever, and the lead credit cards have over actual travel in the way one earns miles. There is simply something nice about credit cards rewards and redemptions which lack in the business travels. No matter how you spin it, those are business expenses and given a choice of your business expense, would you like to conduct business remotely and pocket in the travel expense or actually go thru the travel and pocket measily miles? In 2016, we predict the status quo would be maintained more or less. We will see some exciting offers, some changes, a few bonuses here and there but mostly the same.

Subscribe to:

Posts (Atom)